What happens to debt when you die varies from state to state and is determined by probate laws. Unfortunately, leaving behind credit card and other debt can prevent your heirs and beneficiaries from receiving what you wanted them to have. In some states, your surviving spouse may even have to pay off a portion of your debts!

The best way to avoid this regrettable fate is by ensuring that your Estate Plan and Will are official, appropriately updated, and finalized well before you pass away.

In the event your loved one died with debt or you’re curious for yourself, we’ve got you covered! We break down exactly:

What Happens to Debt After You Die?

When you die with debt, the person named as executor in your Will (aka the person you’ve appointed to handle your affairs) will have to go through the probate process.

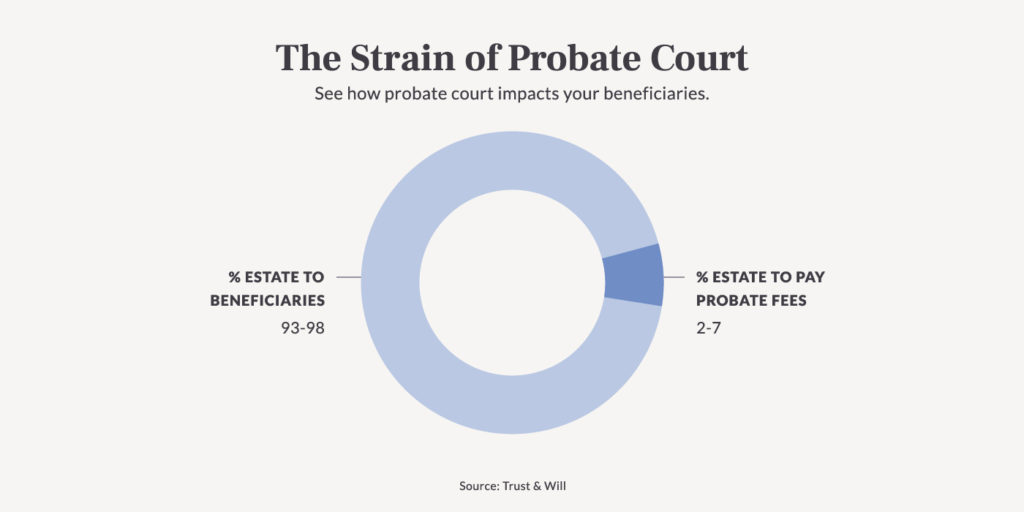

Typically, your estate’s assets (anything from jewelry to artwork to fine china) will be used to pay your outstanding bills. There are some assets that aren’t included in this process because they are not technically owned by your estate (for example, a life insurance policy, IRA, or 401(k)). But for the most part, if you have assets, they will go towards your debts. Unfortunately, this means your beneficiaries will likely receive less than you intended for them in the event you have unpaid debt.

Credit card debt specifically is usually the last debt that is paid back because it is an unsecured debt. A mortgage loan is secured by property, a car loan is secured by the vehicle, etc., and those remaining balances are paid first. Secondly, the estate will often pay for the family’s administrative and legal fees. Finally, unsecured debt (i.e. credit cards) are paid back last. So if your estate doesn’t have enough assets to pay back that credit card debt, the creditors take the loss. Your state’s probate laws will determine exactly what actions are available to creditors — whether that be selling your property or simply having liens placed on the home.

It’s also important to note that creditors have a set period of time in which they are required to file a claim against your estate after you pass (and this deadline varies from state to state).

Can I Avoid Probate?

Yes. There are ways to avoid probate. The best way to do so is by having a Living Trust created before you die. Because the trust “owns” those assets and not your estate, the assets under your Trust are not subject to probate.

Keep in mind that having your assets in a Trust doesn’t necessarily mean you are entirely protected from creditors if you have debt. It just means you’ll have a lot more flexibility compared to what you’d face during probate. With a Trust, your executor has more control and can do their best to negotiate with creditors to (hopefully) reduce your debt. Credit card companies can still sue, but because there are such high upfront costs associated with filing a claim against a person who has died, creditors typically opt for a settlement.

This, of course, highlights the importance of Estate Planning.

Are There Any Exceptions?

Fortunately, it's unlikely that any of your surviving family members will have to use their own money to pay for your debt after you’ve passed. That’s your estate’s job. There are however, a few exceptions:

Cosigner of credit card or loan: In the event you are the cosigner on an account held with a decedent, you would be responsible for paying off the debt on that specific account.

Jointly owned property: Similarly, if you have any jointly owned credit card accounts or property with a decedent, you’d be required to pay the balance on that account or loan.

Community property states: If you live in Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, Wisconsin (or, when special agreements are made, Alaska or Oklahoma), you live in a community property state. In those cases, spouses would be required to pay off anything that was community property: property owned jointly by the married couple.

It’s required by state law: Certain states also may require family members of the decedent to pay debts like health care expenses, or to resolve the estate. In addition, if you were legally responsible for administering the estate and didn’t comply with certain state probate laws, you may have to pay off that portion of the decedent’s debt.

What Should I Do if My Loved One Dies with Debt?

Did you or someone you know have a loved one who recently passed away with debt? Our condolences. We know that the last thing you want to think about is having to deal with your loved one’s affairs and negotiating their debts. But unfortunately, it’s a task that must be completed as soon as possible in order to avoid potential consequences. For example, computer hackers have been known to scour online obituaries in search of identity theft candidates.

That said, here are a few steps that can be taken to ensure your loved one’s debts are managed appropriately:

Know your rights. As we’ve mentioned, probate laws are different in every state. Most require creditors to file a claim within a certain period of time and family members to post a public notice of death before any money can be collected. In addition, The Fair Debt Collection Practices Act (FDCPA) prevents creditors from using unfair or offensive tactics when collecting credit card debt from decedents. Remember, the decedent’s estate is required to pay off their debts starting with secured debts first, so don’t let a collector prey on your emotions in an attempt to get paid first. It can also be helpful to submit a proof of claim request so that you have documentation for your records.

Collect important documents. If your perished loved one kept their important financial documents in a legacy drawer, this step is simple. If not, the surviving spouse can request a copy of the decedent’s credit report. Their credit report will reveal any account on which their name is listed.

Prevent further spending. This may sound obvious, but it’s necessary to ensure that no credit cards in the decedent's name are still in use — even if you’re the authorized user on the card and you want to purchase items related to your loved one’s funeral or burial. Doing so is a sure fire way to complicate things down the line. It’s also smart to be wary of any subscription services the decedent may have held. Recurring payments set on automatic withdrawal can be easily forgotten.

Notify creditors and credit bureaus. Finally, set aside time to call the three most common credit bureaus (Equifax, Experian, and TransUnion) as well as the decedent’s creditors. Start by requesting multiple copies of your loved one’s death certificate so that you can send official notice to creditors and life insurance companies. Next, make the calls (or letters) to necessary creditors and close every account in the decedent’s name. Lastly, reach out to Experian, Equifax, and TransUnion to ask for a “credit freeze”. This will prevent the decedent’s name and accounts from being unlawfully used.

Estate Planning shouldn’t be complicated, expensive, or something you dread. Instead, look at it as something that will provide you and your family comfort knowing that your important affairs will be well taken care of. Dying with debt may not be ideal, but with a thorough Will in place, you can avoid putting your loved ones through additional unnecessary grief and stress.

Share this article